You don't need to be Jumpin' Jack Flash to recognize the state of office space commercial real estate is rapidly changing for the worse.

It's so bad even NPR noticed with an article appropriately headlined "A lot of offices are still empty -- and it's becoming a major risk for the economy".

In this post, I will depart from the topic of geospatial data science to look at what is going on in office space and why it is happening now.

WFH!

Employers reevaluated their need for office space in the pandemic and work-from-home solution.

Footprints were reduced and offices were eliminated in consolidations. Leases weren't renewed. Leases were abandoned. Some businesses went completely out of business. All of that has lead to a 50% vacancy in office space in most major metropolitan centers.

In New York City's Manhattan, 94,000,000 square feet of office space is 'available for lease' -- roughly 139 buildings the size of DTLA's Union Bank Plaza.

Mark to Market Valuations

Enter the world of marketplace valuations.

Simply put, no matter what a seller may think their property is worth based on what they paid for it, the property will only sell to a buyer who sees the same value as a seller's ask. To rephrase it, sellers do the asking and buyers do the offering.

For office space, those perceived values are turning out to be a steep haircut everywhere in the market and a complete shave in some cases.

Speaking of Union Bank Plaza, the historic landmark with plans for adaptive reuse for residential units, sold in March for $104 million -- that's 50% of the $208 million the seller paid for it in 2010. And that's with 62% of the space leased at the time of the sale.

In San Francisco, 350 California Street (a 22 story office tower with 75% vacancy) is expected to sell for 25% or less of its $300 million sale price four years ago.

What an owner paid for a few years ago is now a matter between the owner, their mortgage bank, and oversight regulators should a bank collapse.

One networking contact called it a "sledge-hammer to market" environment. To paraphrase a second contact, why try to catch a falling knife?

A third contact suggested that eventually owners will have to trade at next to nothing in order to escape the expenses of the vacant property that does not produce revenue. For real. The cost of demolishing office space is now a major consideration among buyers.

Why now?

Why is this happening only now? In my opinion, two things.

First, demand went into freefall. It wasn't until the end of most COVID prohibitions earlier this year that the office building sector had a post-COVID snapshot for office space demand.

Second, the cost of money. Rising interest rates mean there's no benefit to refinancing an underperforming property. And, with diminished revenue lenders will pass.

Office Space and Bank Failures

While the post-mortem accounting is still underway, it is highly likely that office space mortgage defaults are driving some banks underwater.

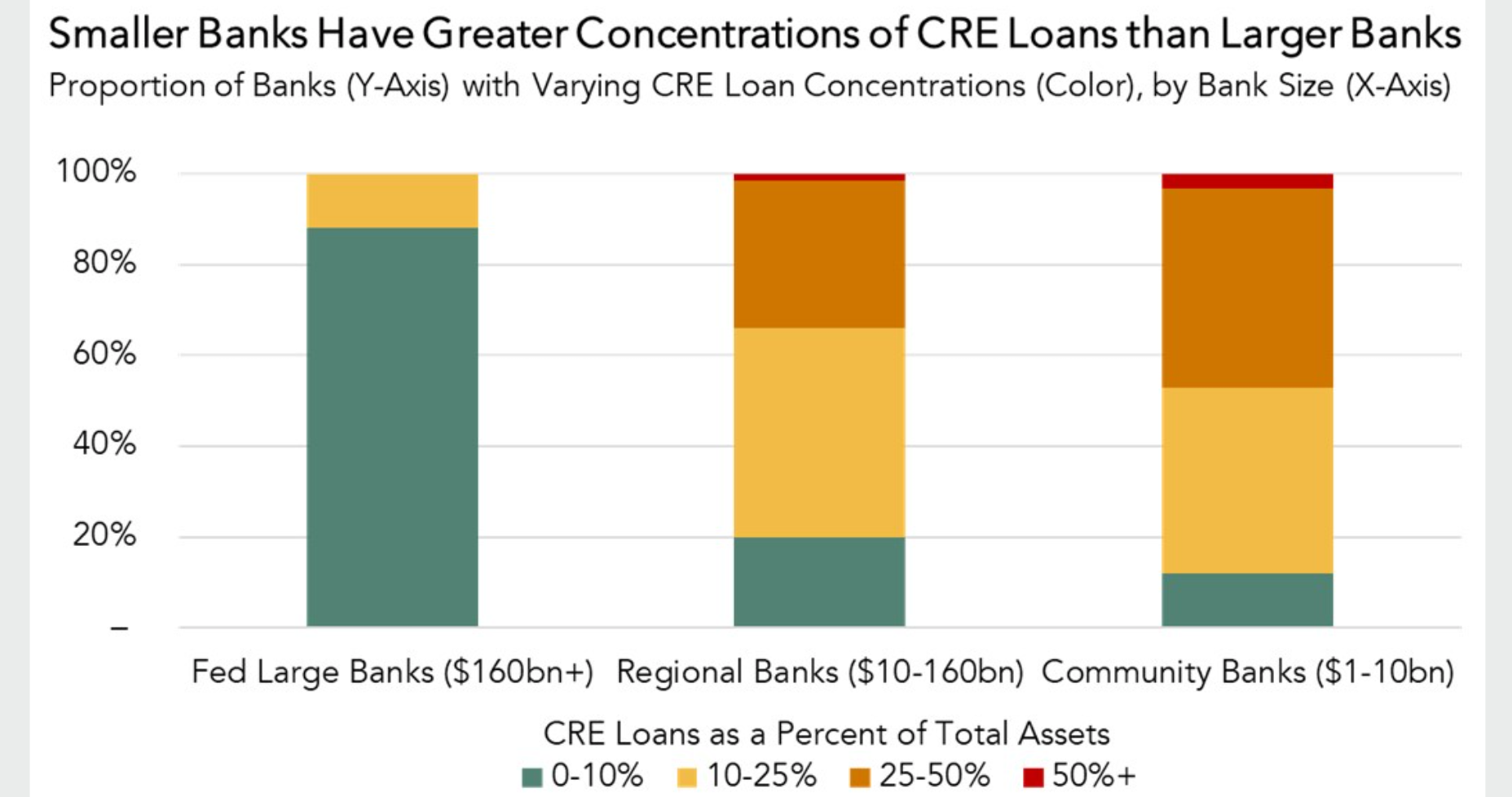

This is because banks, regional and community banks in particular, are the primary lenders for commercial office space mortgages.

Federal Reserve data indicates small and midsized banks hold 67.2% of all commercial real estate loans:

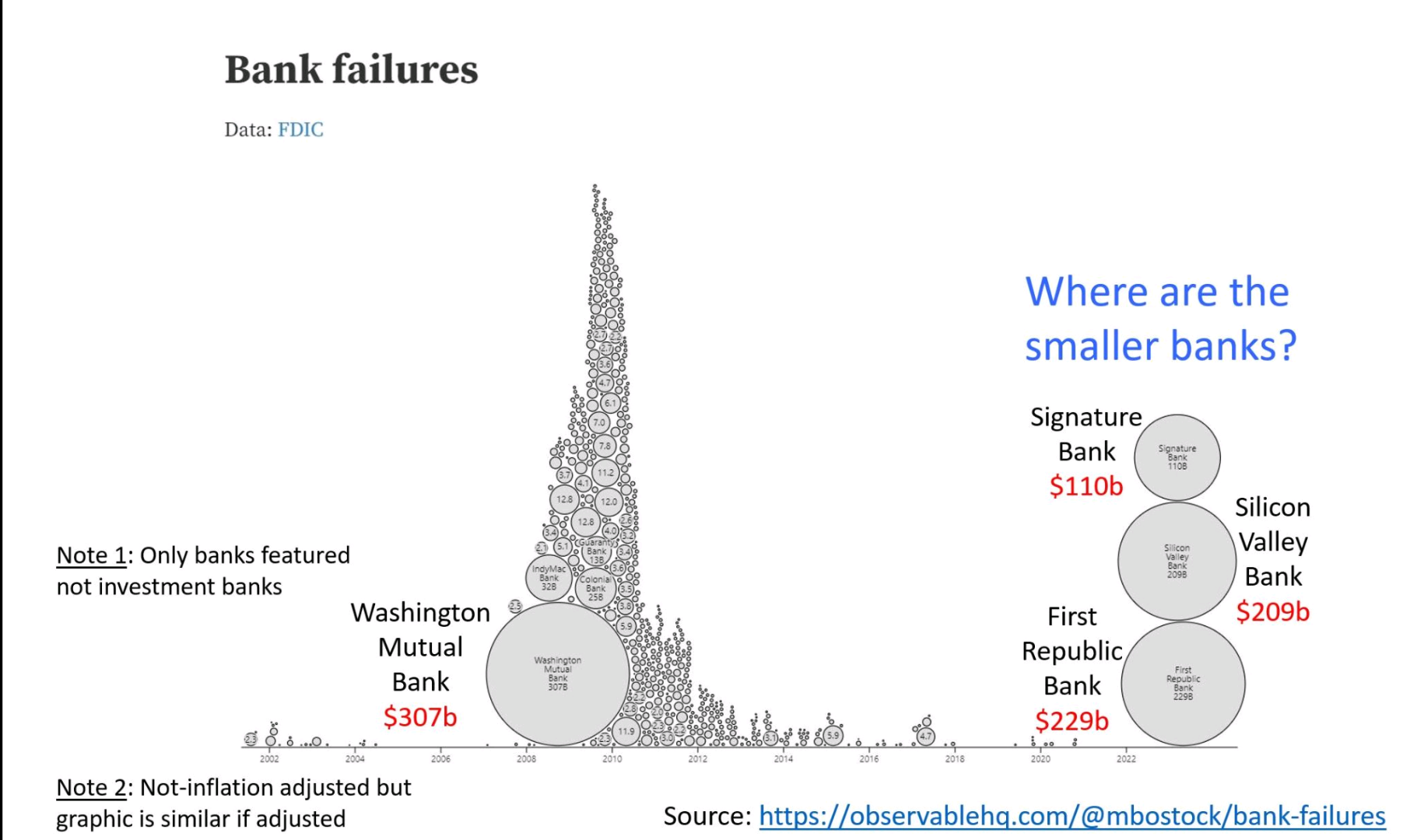

Three recent bank failures, two large banks and one regional, were collectively $548 billion -- almost twice the size of the Washington Mutual's $307 billion collapse in 2008. First Republic Bank was well known for its lending on office space in San Francisco and Signature Bank for its lending on office space in New York City.

Top-shelf operators are not immune from defaults, delinquencies, and troubles.

Brookfield defaulted on $765 million in loans on two DTLA office towers -- The Gas Company Tower and 777 Fig -- earlier this year. And Brookfield is reportedly delinquent on a $275 million loan tied to EY Plaza, also in DTLA.

Onni is reportedly in trouble with a $408 million loan on the Wilshire Courtyard office complex in LA's Miracle Mile (a site the size of two city blocks).

What about adaptive reuse?

If you think residential conversion are going to save the day, please don't hold your breath.

Residential conversions are hard and expensive. Existing floorplans and existing mechanicals plus the cost of individual electrical, plumbing, and HVAC all mean major capital investments in material and labor. With a bottom not yet reached, re-developers will be reluctant to move on all but the most lucrative opportunities. Capital providers will also be reticent to embrace financing adaptive reuse conversion projects knowing that new construction is often more cost effective than adaptive reuse as well as more sought after by the marketplace of renters.

There are other ideas. These examples require minimal renovations and potentially provide revenue faster than the timeline of a residential adaptation or complete demolition and rebuilding of residential space.

One Wilshire did not start out as a major data center. The building was initially occupied by law firms.

When telecoms moved into the building, it's connectivity infrastructure was updated. As more and more hardware moved into the location, additional HVAC capacity was installed to manage the heat given off by servers. Today, because of its telecom tenants, One Wilshire is said to be 'the hub' of the internet in the Pacific Rim. Not every building can become a global hub, but the need for more data centers persists.

Climate controlled mini-storage is another idea. In Los Angeles, that will likely require a change to the existing zoning regulations that apply to most office space. There's also a form of controlled environment agriculture known as vertical farming. Global food supplies remain a major concern and this may be, no pun intended, a growth area for potential reuse.

The Bottom-line

Keep calm and carry-on in adaptive, inventive, and resilient ways.